The latest analysis from Circana examines ice cream in convenience in terms of value sales and market share

Given the poor summer of 2023, it is not surprising that Ice Cream value sales, albeit still in growth, have slowed compared to the food market in total and the overall frozen category.

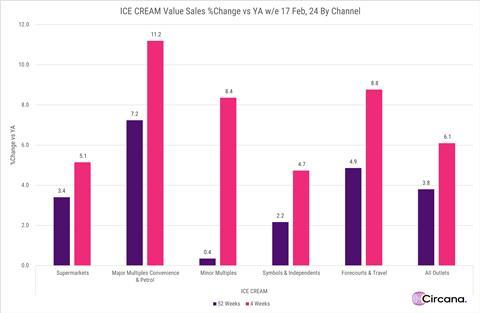

Ice cream in the last 12 months to Feb 17 2024 is up by 3.8% on last year, but frozen sales are up 9.3% and food sales up 7.2%, meaning that Ice Cream has lost value share over the last 12 months.

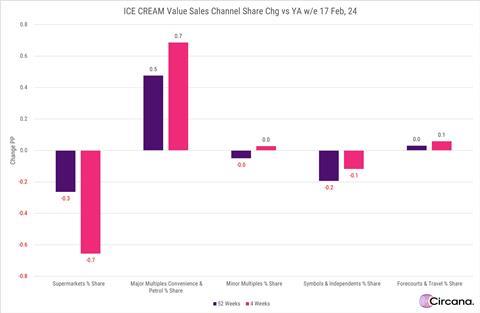

However, what is more surprising is the relative performance of the channels across the last year. With a poor summer, we’d expect less people to be out and about and as a result convenience to lose share versus last year and indeed symbol and independent convenience has lost 0.2 percentage points (PPs) of value share over the last 12 months, but counter-intuitively major multiple grocer convenience has gained significant share, up 0.5PPs in the last 12 months, winning share from supermarkets which were down by 0.3PP versus last year.

Oddly, the trends looks to be accelerating in recent periods with 0.7PP swing from supermarkets to major multiple grocer convenience in the latest four weeks, with symbols and independents value share loss also slowing to just of 0.1PP down in the last four weeks, all of which is difficult to rationalise given the rainy weather since the turn of the year.

What’s next in Ice Cream?

It’s no surprise that the Ice Cream category does better in warmer weather so as we approach summer, sales will hopefully improve. Ice Cream falls under HFSS regulations and this will be the second year of this legislation being in effect so retailers will have had a full cycle of seasonal events to adapt to any changes. With sales in the category moving towards major multiple managed grocery convenience outlets, it shows that consumers are still attracted to the category but it may be part of a broader shopping mission rather than the sole focus of a store visit. Retailers should be looking to disrupt shoppers with their Ice Cream fixture rather than banking on it to attract customers in on its own, all while making sure they stick to legislation that might affect the category.

No comments yet