Demand amongst shoppers across six key European markets is unlikely to recover until the second half of 2024, new research has found.

Published by Circana, the report, ‘FMCG’s Race for Resilience: Unlocking Growth’, highlighted how shoppers in France, UK, Germany, Italy, Spain and Netherlands are continuing to buy less with unit sales down −1.3% over the past year despite inflation driving FMCG value sales up by 10.1% year-on-year to reach €636bn.

Circana global SVP of strategic growth insights Ananda Roy said demand hasn’t returned to pre-pandemic levels. “Two years post-pandemic and the FMCG sector remains far from normal,” he said. “Demand has yet to fully recover and we see more everyday categories becoming discretionary. Private labels continue to gain share from brands, and inflation-fatigued consumers are coping by buying on deal and shopping at the discounters. As global turmoil and uncertainty continue, we expect that FMCG demand will not recover before the second half of 2024.”

He goes on to say that there is potential for a return to volume growth. “The good news is that a return to volume growth is possible and a clear playbook is emerging for how to achieve it. Growth and opportunity exists in the areas of innovation, sustainability and pricing, boosting resilience to future shocks.”

Frozen category success

Roy highlighted the frozen category as one for growth. ”Frozen is one of the big winners – With the cost-of-living crisis helping this category to becomean ‘everyday’ purchase for European consumers who wouldn’t have considered buying it in thepast. Five of the top 20 biggest-selling food categories are now frozen: frozen potatoes, frozenmeat, frozen snacks, frozen meals and frozen bakery.”

Private label growth

The report also found that brands are losing further ground to private labels. It revealed that private label accounts for 39% of grocery sales in the EU6, and is worth €246bn to retailers, having grown its value share by a further 2.2 percentage points in the last year (to June 2023).

“High inflation has acted as a catalyst for private label growth, but its success is not due to cheaper prices alone,” said Roy. “Private label has become even more premium in recent months and as a result, the price gap between private label and national brands has shrunk - now averaging 15-20% in food categories, down from 28-40% two years ago.”

The Circana report did add that there will be a limit to private label growth and that while ”retailers want private label to compete with vigorously with brands, they don’t want brands to fail” as they are the biggest driver of value, innovation and footfall in European retail.

The research issued a warning that entire categories could become ‘innovation deserts’, with a 22% drop in new launches coming to market in the six markets over the past year.

It found that less than 1% of NPD represents breakthrough, new-to-world or new-to-category innovation, with the overwhelming majority being existing products that have been renovated, reformulated, repackaged or – increasingly – ‘shrinkflated’ and relaunched with new EAN codes. There has been a small number of innovation ‘superstars’ accounting for 56% of value and 40% of unit growth generated by NPD over the past year, with the UK in particular over-indexing on such superstars, with 33% of all superstar launches originating in the UK.

Commenting on this reported lack of innovation, Roy added: “Brands are understandably cautious about placing bets on risky, new-to-market NPD in the current climate,but retreating from NPD would be seriously short-sighted. The most enterprising brands are already zeroing in on the opportunity from the turmoil and finding new ways to drive demand.”

Dynamic pricing

One area of opportunity for the convenience channel highlighted by the report was dynamic pricing. With the roll-out of electronic shelf-edge labelling, dynamic pricing is easier to implement, particularly for convenience retailers who have more control over merchandising. It did warn that any retailer who is planning to introduce needs to be very sure of customer reactions beforehand especially regarding accusations of profiteering and greedflation.

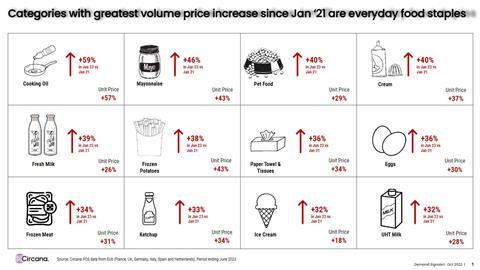

What products have increased most in price since Janary 2021?

No comments yet