Premium chocolate is growing nearly 20% faster than mainstream: yet four in five convenience shoppers who buy it are buying it somewhere else. The data is clear. So why isn’t the fixture catching up?

Walk into most convenience stores and the chocolate shelf tells a familiar story. The front-runners are the same brands that dominated the category a decade ago, arrayed in familiar formats at familiar price points, optimised for habitual consumption. The implicit assumption is the convenience shopper wants volume, speed and value. Increasingly, the data indicates otherwise.

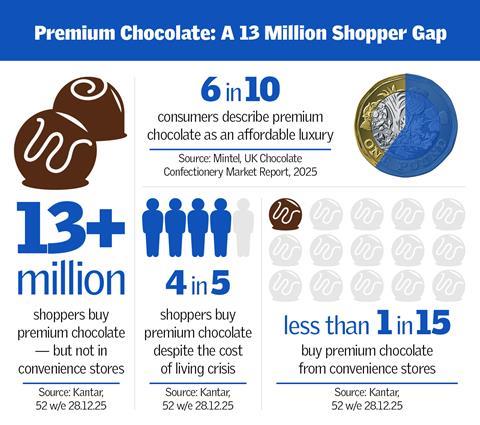

Over the past five years, premium chocolate has grown nearly 20% faster than mainstream – 9.3% annual growth versus 7.9% [Circana]. Premium now commands nearly a third of total confectionery market value [Mordor Intelligence, 2025], a share that has risen steadily even as volume growth has flattened. Shoppers are not buying more chocolate; they are buying less of it, but care considerably more about what they get for their money. Six in ten now describe premium as an affordable luxury, even under financial pressure [Mintel, UK Chocolate Confectionery Market Report, 2025].

The commercial implication is compelling. Kantar data shows 60% of UK shoppers use convenience stores, and four in five buy premium chocolate somewhere in the market. But fewer than one in 15 are buying it from a convenience store [Kantar]. That gap represents more than 13 million shoppers who could convert their premium purchase to the channel – but currently don’t.

“Premium chocolate is growing faster in the market. Shoppers are buying it in the market, but they’re not buying it in a convenience store”

– Alex Hillhouse, convenience category controller, Lindt

A structural problem – and a supplier one

The distribution numbers make the gap concrete. Mainstream single countlines have 86% distribution across convenience stores; premium countlines just 30%. For bars: mainstream at 54%, premium at 15% [Circana]. The category is present in almost every store in the country. The premium tier is present in almost none of them.

Patrick Mitchell-Fox, retail insight partner at IGD, puts the context plainly. “Overall confectionery makes up about 7% of total convenience sales and grew at 4.1% last year,” he says. “Premium tablet chocolate has a place in plenty of stores but that presence is likely to vary quite widely according to location and catchment. The challenge with convenience is always space – every product needs a very strong reason to be there.”

Alex Hillhouse, convenience category controller at Lindt, is clear-eyed about why that case isn’t being made consistently. “The route to market is fragmented,” he says. “Category advice and shopper-led decisions get diluted as they go down. A lot of decisions in stores are based on commercial priorities – and there’s a lot of activity that incentivises retailers to carry a broad range of certain things, where actually that duplication might not be adding additional transactions or bigger baskets.” He also points to supplier-side blockers Lindt has been working to remove: case sizes requiring too much outlay, pack formats wrong for convenience, and the absence of price-marked packs (PMPs), which account for 80% of volume through some stores.

The contrast with gifting is instructive – where boxed premium chocolate has 39% convenience distribution versus 59% for mainstream [Circana]. Retailers understand the premium story when it’s framed as gifting. “They get the story in the smaller part of the market,” says Hillhouse. “What we need to do is demonstrate there is rate of sale on the missions which make up three-quarters of occasions in convenience – for me and for sharing.”

The ‘8pm treat’: a luxury-hunting mission

Lumina Intelligence data shows the treat mission now accounts for 30.3% of all chocolate purchases in convenience – up 2.4 percentage points year on year and now the single largest purchase occasion for the category [Lumina]. Quality as a purchase driver has risen 4.2 points in a year, individual bars are up 5.5 points as the preferred format, and share bags are declining sharply. Lindt’s own Polaris research adds a further dimension: three-quarters of convenience shoppers are looking for chocolate as a snack or dessert replacement, with the single biggest untapped need state being a moment of indulgence [Lindt Polaris, 2021].

Flora Zwolinski, insight lead at Lumina Intelligence, says the treat mission is becoming harder to pin down – and that is precisely what makes it an opportunity. “Treat can mean lots of different things to lots of different people,” she says. “There’s now an element of trading up to a more quality-driven, higher-priced premium chocolate – and actually there’s sometimes a part of you that feels good, perhaps a perception that higher-quality brands have better ingredients and are therefore less ultra-processed.” She adds that price itself has become a quality signal: “If something’s high price, it’s perceived as more premium. The first taste is with your eyes.”

Mitchell-Fox agrees the missions framework is key. “Evening in is clearly a mission convenience retailers have in mind – sharing snacks and sharing confectionery often sited adjacent to alcohol,” he says. Yet most stores are not set up for it. Hillhouse observes the evolution underway in convenience – coffee machines, food-to-go, the hot lunchtime offer – is largely focused on the daytime. “They then don’t shift that around the evening, for someone on their way home.

“Think about the need states of how they are at that time. They’re on their way home. They’re not on a big shop mission. If you signpost or offer something that meets that need, in that transient moment, you’re likely to get a conversion.”

Lumina’s tracking data reinforces this. “I saw it and was tempted” now accounts for 51.6% of all chocolate impulse purchases in convenience, up three percentage points year on year [Lumina] – showing resilience despite HFSS placement restrictions. Zwolinski attributes this in part to the visual impact of newer premium brands. “What’s driving it now are vibrant-looking premium brands with bold, design-led branding that catches people’s eyes,” she says. “The premium end is certainly starting to convert that impulse moment more. And consumers really do like choice.”

The margin case – and the trial that pays off

Retailers who have tried a credible premium range tend to see it work. Outside London – where retailers might assume premium is too aspirational – the rate of sale for premium lines is competitive against category benchmarks where distribution exists. The barrier is not the shopper; it is the decision to stock.

The financial case is not framed as a choice between premium and mainstream. “Mainstream is there for frequency,” says Hillhouse. “Premium is there to drive value trade-up and basket size. You have to offer both ends of the market.” Premium lines offer competitive cash margin without needing the same volume churn as mainstream – which matters in a channel where transaction frequency is declining. Hillhouse points to Londis in Coulsdon, where the owner trialled premium options across categories previously dismissed as wrong for the store and saw them deliver, and to Go Local Extra in Southampton, which has refitted and given space to premium chocolate lines.

Many independent convenience stores fall below the square footage threshold at which HFSS placement restrictions apply, giving them more flexibility than larger stores. Even where restrictions do apply, the issue is rarely legislation – it is duplication. There is already enough confectionery space in most stores that carving out a small area for premium does not require a refit.

“Confectionery holds a lot of space in a lot of stores. With some more considered choices on just a small proportion of that space, retailers can benefit from increased transaction value, cash margin and shoppers who are happier with an offering that meets more of the missions they are on,” observes Hillhouse.

What a premium-optimised fixture looks like

The mechanics are not complicated. A curated range of five to eight premium lines – consistently stocked, visibly signposted, with secondary siting near the till or adjacent to a coffee-to-go offer – is a meaningfully different proposition from a token premium line wedged between mainstream bars. Seasonal occasions – Easter, Valentine’s, Christmas – represent the lowest-friction entry point; the gifting logic is already understood, it is a matter of executing it consistently and early.

Symbol groups and wholesalers are increasingly providing the support to make this easier. “I’ve definitely seen far more support from wholesalers and symbol groups to help these convenience retailers be more consistent in their execution,” says Hillhouse. “They have the opportunity now to trial things that will meet an occasion like the 8pm treat – because they’re getting more support on how their stores show up.”

The retailers winning right now are not doing anything exotic. They are ranging a tight premium core, keeping it visible and giving it secondary siting. The data is there, the shopper appetite is there, and the supplier and wholesale support is increasingly there too. The stores that act on this will not merely capture incremental confectionery sales: they will signal to a higher-spending shopper they are a store worth choosing.

For more information, please visit: https://www.lindt.co.uk/

The GLP-1 effect — a new kind of chocolate shopper

According to Lumina Intelligence’s GLP-1 Tracking data, 4.7% of UK adults are currently using GLP-1 weight-loss medications such as Ozempic or Wegovy, with a further 9.6% considering it [Lumina]. Current users are disproportionately ABC1, aged 25-44 and London-weighted – around 44% fall into this affluent millennial bracket, with nearly one in four having a household income above £100k. Critically, this group over-indexes on convenience store visits.

The dietary logic initially looks challenging for confectionery – GLP-1 suppresses appetite and reduces snack frequency. But Zwolinski urges retailers not to treat all GLP-1 users as a single story. “If you’re in an affluent area with a lot of millennials, smaller, high-quality premium formats will cater to people on GLP-1,” she says. “But a lot of what those shoppers want – nutrient-rich, portion-controlled product – also appeals to health-conscious consumers not taking the drug. So there’s a meaningful overlap.” For the time being it is very much a know-your-catchment opportunity – but as NHS pill-format rollout broadens access, the demographic will shift. The window to get ahead of this shopper is now.